Reincorporating Your Non-US Startup in the U.S. through the “Delaware Flip”

Imagine that you are the founder of a Brazilian B2B SaaS startup that has landed a few enterprise clients and has some good traction. Your sights are now set on raising capital in Silicon Valley to scale your business and reach new markets. While your conversations with U.S. based investors are productive, you soon realize that they are unwilling to invest in your Brazilian startup as it is governed by laws they are not familiar with. The U.S. investors request that your company re-incorporate in the State of Delaware.

This is the reality for many non-U.S. startups seeking American venture funding. This article explains the transaction that is known as the “Delaware Flip” and what is involved in reorganizing your company in the U.S.

Reincorporate in Delaware to Access to U.S. Capital

The amount of venture capital coming from the United States surpasses the rest of the world in total investment dollars and U.S. investors are the primary source of funding for many non-U.S. tech companies. Wherever your startup is located internationally, the investment climate may not be as favorable for your company as it is in America even if your business model is sound. Additionally, U.S. investors can provide the connections and expertise to help scale your business and facilitate the entrance or expansion of your company’s products or services in the U.S. market. Incorporation in the U.S. may also facilitate a company’s future exit opportunities through acquisition or the public market as there are more startup exits in the U.S., generally at higher valuations. Finally, a non-U.S. tech company doing business in a competitive labor market cannot offer its employees the same equity compensation benefits and potential payout that a U.S. company can, which can leave a non-U.S. company at a disadvantage when competing for talent. Although this may change in the future, these are all legitimate reasons why a non-U.S startup would want to raise capital from U.S. investors.

However, there is a caveat; Most VCs and sophisticated investors prefer to invest in U.S. companies because they are more familiar with the legal and regulatory regime and most will only invest in companies that are specifically incorporated in the State of Delaware. There are many good reasons for this requirement. For one, Delaware has a well-developed body of law favorable to shareholders of corporations and provides investors with a certain level of predictability when carrying out investment transactions. If a Delaware company becomes involved in litigation, investors know that the judge will be familiar with complex corporate law matters. U.S. VCs are generally unwilling to invest in companies incorporated outside the U.S. as the laws and regulations of other countries are unfamiliar to them and their counsel and may not allow for the standard rights and control mechanisms typically contained in U.S. VC term sheets, including anti-dilution or redemption rights, or the right to a board seat. Additionally, should any issues arise, it would be very expensive for the VC firm to have to hire counsel in a foreign country and possibly be required to travel there themselves.

Get the guidance you need when setting up your company for investment.

Explaining The Delaware Flip

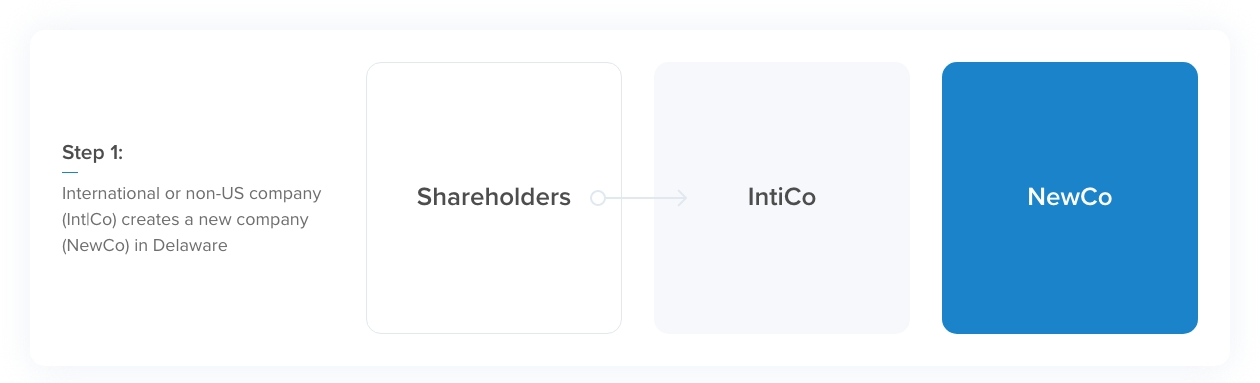

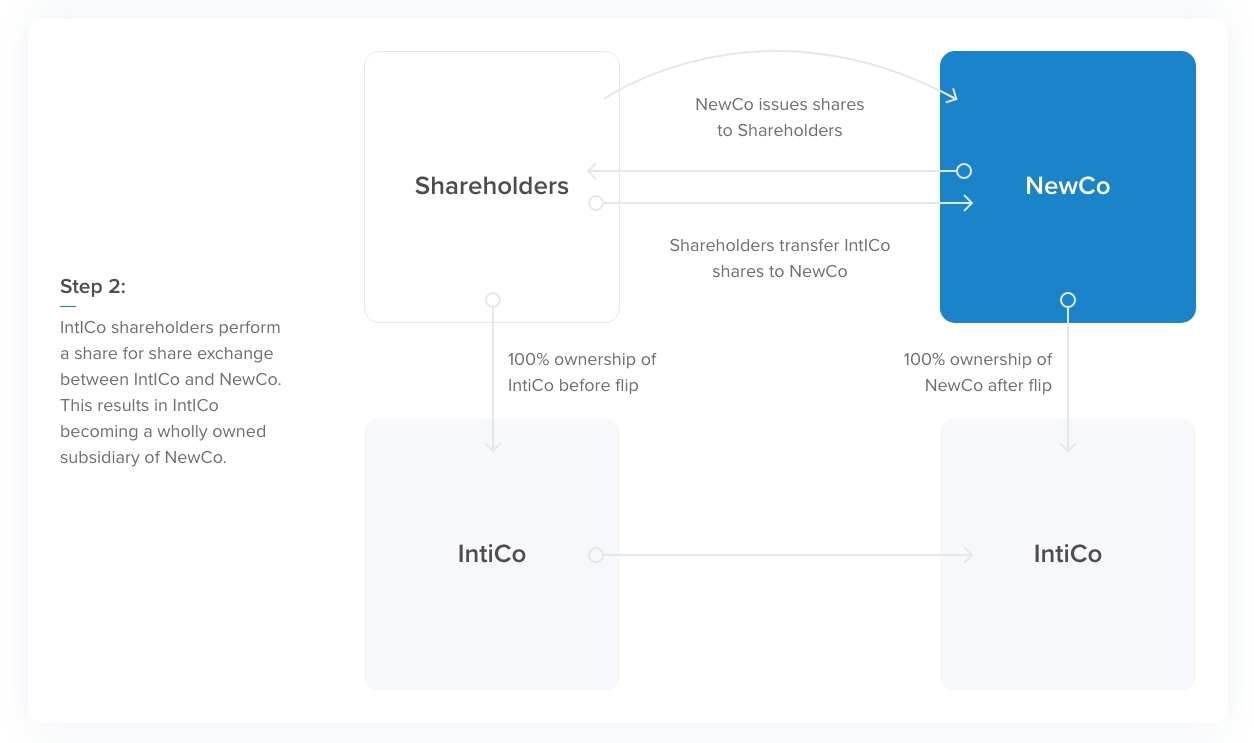

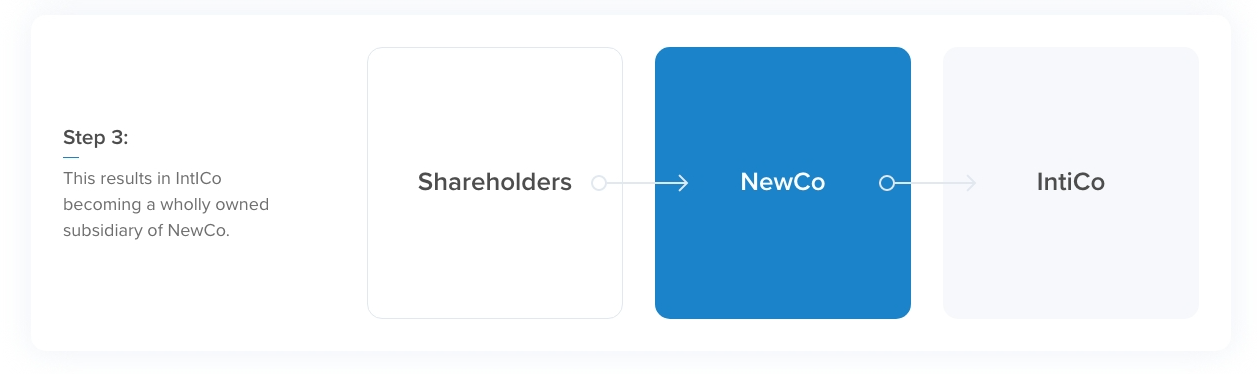

A Delaware Flip is the term for the process of reorganizing a non-US company’s corporate legal structure into a US legal structure under the laws of the State of Delaware. To effectuate a Delaware Flip, the non-US company would form a new corporation in Delaware as a holding company. Thereafter, through a share exchange agreement or similar agreement, a share-for-share exchange is effectuated, which results in the non-US company becoming a wholly owned subsidiary of the new Delaware corporation. The U.S. investors then invest in the parent Delaware company which will initially have no operations and its sole asset will be 100% of the non-U.S. company. Eventually, any operations not located in the original non-U.S. country will likely be performed through the parent Delaware company.

Note that depending on the jurisdiction of the non-U.S. country, the share exchange process may be more complex and there may be registrations required in the non-U.S. country. For this reason, you should work with both counsel in the U.S. and the original country of incorporation to properly structure the new Delaware company and to properly effectuate the share exchange.

Tax Implications of a Delaware Flip

If structured properly, the transaction may be tax neutral for both the non-U.S. company and its existing shareholders. Any existing tax benefits enjoyed by the non-U.S. company and its shareholders should generally be preserved to the extent possible.

After the Flip, the new Delaware company will be subject to both federal and state corporate taxes, which may be higher or lower than the taxes in the non-U.S. jurisdiction. The non-U.S. subsidiary will be considered a “controlled foreign corporation” of the Delaware parent company and need to be included in the U.S. tax statement of the U.S. company. If the non-U.S. jurisdiction has a double taxation treaty with the U.S., then the income of the non-U.S. subsidiary’s shareholders may be eligible to be taxed at a reduced rate (varies by country) or exempt from U.S. income taxes and instead taxed in its own jurisdiction. Note that U.S. states are independent in their taxing authority and some states do not honor the provisions of U.S. tax treaties. If there is no tax treaty between the U.S. and the non-U.S. jurisdiction, the non-U.S. shareholders must pay income tax in the same way and at the same rate as a Nonresident Alien.

Because there are so many variables concerning tax treatment of the share exchange transaction and income depending on the non-U.S. jurisdiction, it is extremely important to work with tax experts on the implications of a Delaware Flip. Additionally, individual shareholders of the non-U.S. company should seek independent tax counsel.

Why Would a Non-U.S. Company Not Want to Perform a Delaware Flip?

Tax Consequences: One of the leading reasons why a non-U.S. company would not want to perform a Delaware Flip (or reincorporation in any other country or U.S. state), is due to the potential tax implications. The tax issues for a Delaware flip can become very complicated, especially for larger companies. Companies could inadvertently trigger adverse tax consequences when transferring assets and lose more than they gain. A failure to comply with the rules and requirements of the jurisdictions may result in a tax event, the loss of valuable tax benefits or other adverse financial consequences.

Additionally, you may want to wait to perform a Delaware Flip until you are positive that your startup can obtain capital from U.S. investors as undoing the Flip may have undesirable U.S. tax consequences.

Government Fees: Although there are benefits, such as faster filing processes and a sophisticated court system, a company that is incorporated in Delaware must also pay for a registered agent, register a foreign qualification in any other state in which it does a substantial amount of business or has a physical location, pay franchise taxes, and comply with annual reporting requirements separate from its home jurisdiction.

Subject to U.S. Laws: The company will also be subject to Delaware corporate law. A startup that is small, early in its lifecycle, and/or not physically in the U.S. may find that the costs of the transaction and its long-term effects outweigh the benefits. As a company grows and its capital structure and commercial relationships become more complicated, the process of reincorporating becomes more complex. A company may also desire to remain outside of US jurisdiction because it currently does not

comply with the specifics of U.S. laws.

Despite the potential issues that arise with a Delaware Flip, the access to U.S. capital and markets may far outweigh the transaction and compliance costs and provide a significant increase in shareholder value over the long term. If you are considering reincorporating your non-U.S. company in the U.S., it is best to consult with experienced counsel to navigate the complexities of this transaction. Experienced counsel will discuss the different legal considerations with you and help you determine the best strategy moving forward. SPZ Legal, P.C. has performed Delaware Flips for its non-U.S. clients and will take the time to understand your business needs and tailor any advice to fit your short-term and long-term goals.

About

David De La Flor is a business law attorney at SPZ Legal, P.C., where he takes great pride in the achievements of his clients. With a firm belief that entrepreneurs and companies of all sizes deserve exceptional legal counsel, David is committed to delivering personalized attention to each client. His affiliation with Gust Launch’s Startup Legal Counsel network exemplifies his dedication to providing comprehensive support to startups and emerging businesses.

Get the guidance you need when setting up your company for investment.

This article is intended for informational purposes only, and doesn't constitute tax, accounting, or legal advice. Everyone's situation is different! For advice in light of your unique circumstances, consult a tax advisor, accountant, or lawyer.