Craft a Lean Business Plan to Serve as Your Venture’s Roadmap

[The following is an edited excerpt from David S Rose’s book The Startup Checklist: 25 Steps to a Scalable, High-Growth Business.]

Mention the term “business plan” and the image that likely comes to mind is a thick document generated by a business consultant for you to give to a banker or investor and then forget about. But since these days everyone worships at the altar of the lean startup, it’s common knowledge that a business plan is “old school” and completely useless. All you need is a slide deck and a great team, right?

Wrong! That’s because, while you weren’t looking, the old school business plan was superseded by something that is critically important, intended for you instead of other people, developed by you instead of other people, and constantly reviewed and updated. It is called “The Lean Business Plan,” and in this chapter I will (with permission) borrow liberally from the work of Tim Berry—the world’s leading expert on business planning—to give you a quick overview. For a complete hands-on lesson, you will want to read Tim’s definitive book, The Lean Business Plan, which is available both in book form and for free as a series of detailed posts on his website.

The Principles of Lean Business Planning

1. Do Only What You’ll Use.

Lean business means avoiding waste and doing only what has value. That means starting with a lean plan instead of a giant document, and continuing with a planning process involving regular review and revision. You keep it lean because it’s easier, better, and, in practice, is really all you’re going to use.

The lean plan is about what is supposed to happen, when it is supposed to happen, who does what, how much it costs, and how much money it generates. It’s a collection of decisions, lists, and forecasts that doesn’t necessarily exist as a single document somewhere. You use it to track performance against your plan, review your results, and revise regularly so the plan is always up to date. It will be more useful if it’s gathered into a single place, but it doesn’t have to be. And it’s only as big as you need for its business function.

The main output—and therefore the main purpose—of the lean business plan is a better business. Forget the additional descriptions and verbiage for outsiders until you need them. Wait for that until you have what Tim calls a “Business Plan Event ,” where someone else needs to understand where you’re going. At that point, you can take your core, updated plan and add a small bit of contextual and formatting material, and you’ll be all set.

You need to know your market extremely well to run your business. What you do not have to do, however, is include everything you know about it in your lean business plan.

Your lean plan is about what’s going to happen, and what you are going to do. It’s about business strategy, specific milestones, dates, deadlines, forecasts of sales and expenses, and so forth. It’s not a term paper.

2. It’s a Continuous Process, Not Just a Plan.

Lean business planning isn’t about a plan that you do once. Just like lean manufacturing and lean startups, it’s a process of continuous improvement.

With lean planning, your business plan is always a fresh, current version. You never finish a business plan, heave a sigh of relief, and congratulate yourself that you’ll never have to do that again. With lean planning, the plan is smaller and streamlined so you can update it easily and often, at least once a month. Your lean plan is much more useful than a static plan because it is always current, always being tracked and reviewed, frequently revised, and a valuable tool for managing.

Because of this, a business plan is not a single thing. It’s not something you can buy, or find pre-written. You don’t do it and forget it, and you can’t have one written for you. If you don’t know your plan intimately, then you don’t have a plan.

Get the guidance you need when setting up your company for investment.

3. It Assumes Constant Change.

One of the biggest and most pervasive myths about planning is that it reduces flexibility. In fact, when done the right way, it builds flexibility. Lean business planning manages change. It is not threatened by change.

Running a business effectively requires minding the details but also watching the horizon. It’s a matter of keeping your eyes up (looking at what’s happening on the field around you) and your eyes down (dealing with the ball), both at the same time.

4. It Empowers Accountability.

It is much easier to be friends with your coworkers than to manage them well. Every startup founder has to deal with the problem of management and accountability. Lean business planning sets clear expectations and then follows up on results. It compares results with expectations. People on a team are held accountable only if management actually does the work of tracking results and communicating them, after the fact, to those responsible.

In good teams, the negative feedback is in the metric itself. Nobody has to scold or lecture, because the team participated in generating the plan, and the team reviews it. Good performances make people proud and happy, and bad performances make people embarrassed. It happens automatically.

It is important, however, to avoid the “crystal ball and chain.” Sometimes—actually, often—metrics go sour because assumptions have changed or unforeseen events happen. You need to manage these times collaboratively, separating the report from the results. Your team members will see that and believe in the process, and continue to contribute.

5. It’s Planning, Not Accounting.

One of the most common errors in business planning is confusing planning with accounting, and this is true for lean planning too. Although they look like accounting statements, your projections are just projections. They are always going to be off, one way or another. The purpose of projections isn’t to guess the future perfectly, but rather to set down expectations and then connect the links between spending and revenue. Think of it like this: accounting goes from today backwards in time, in exact detail. Planning goes forward into the future, in ever-increasing summary and aggregation.

The reports that come out of accounting—called statements—must accurately summarize the actual transactions that happened in the past. But projections, unlike financial statements, are just educated guesses about the future. They aren’t reports of a database of actual transactions. Where accounting reports on records in a database, for projections, we guess what the totals might be.

So don’t try to imagine all the separate future transactions in your head and then report on them. You estimate the totals. That’s not only easier, but better as well. It’s a better match to how the projections help you manage, and how we humans deal with numbers.

How to Make a Lean Business Plan

1. Set Your Strategy.

If you’ve been following along in this book so far, you will be well on your way to having defined your venture’s strategy, because that’s what you worked through in the last chapter with the Business Model Canvas.

You should now have a clear focus on the core of your business that will be used as the context as opportunities arise and decisions need to be made. It is in our entrepreneurial DNA to want to go into every new market to please everyone we can. But a good strategy summary helps to frame new opportunities correctly, and without emotion.

Finally, the strategy as it currently stands, as well as any potential revisions in response to real-world conditions, should be reviewed in the monthly review sessions that are an integrated part of lean business planning.

2.Plan Your Tactics to Implement the Strategy.

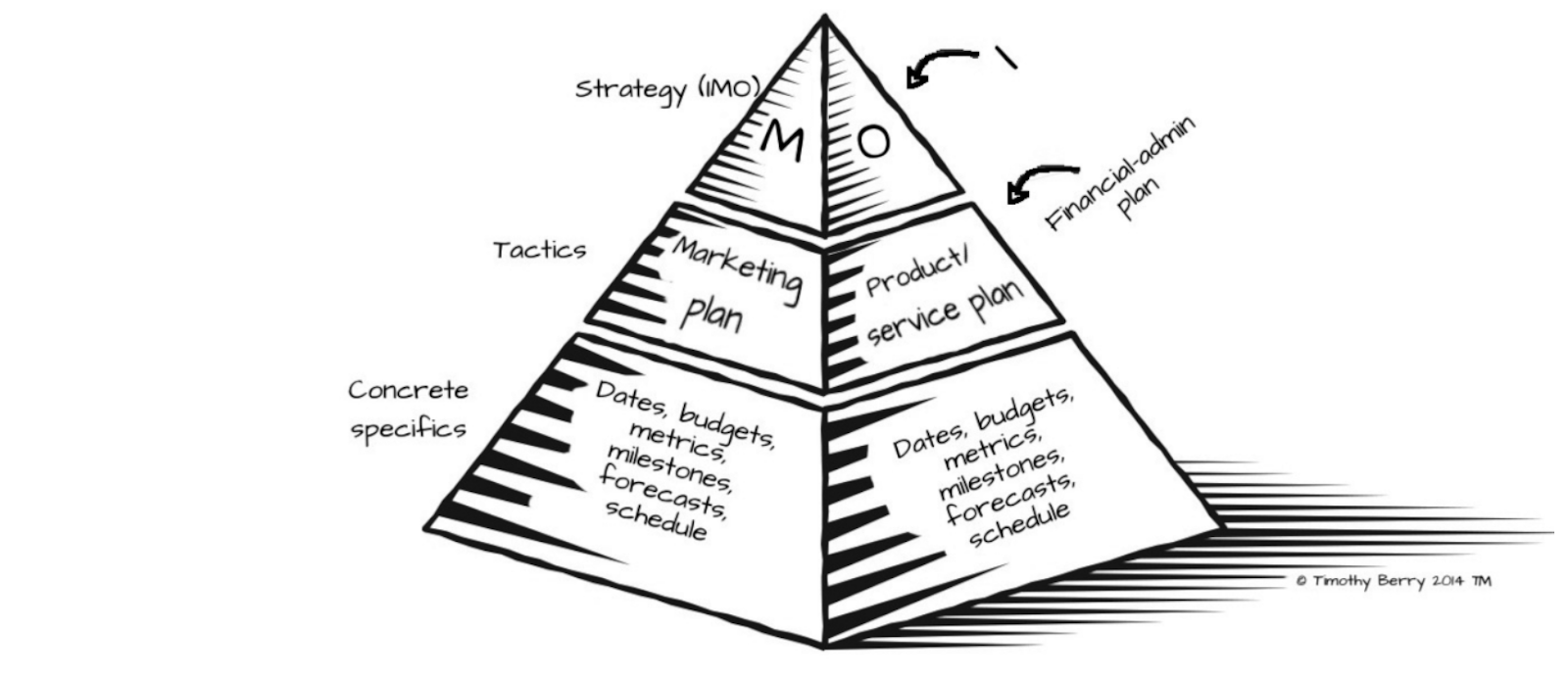

You should think of your business plan as a pyramid, with strategy at the top, tactics in the middle, and concrete specifics at the base. The middle of the pyramid, which connects the Why’s to the What’s, are your tactical plan.

When it comes to your lean plan, these tactics should be as simple as possible—ideally just bullet point references. Don’t worry about writing descriptions and explanations or compiling background information until you have a real business need to explain them to outsiders. Do worry about thinking through all of your marketing and product plans, and planning them well.

Figure 2.1 – Lean Plan Pyramid

Marketing Tactics. Marketing, in its essence, is getting your customers to know, like, and trust you. To do that, you must understand them inside and out. Know how and where to find them, how to help them find you, and how to present your business to them in the way that best matches your strategy and business offering. You have to make choices about pricing, messaging, distribution channels, social media, sales activities, and so forth. For your lean plan, these are mainly bullet points—for your internal use only.

Product/Service Tactics. Product and service tactics are the decisions you make about pricing, packaging, service specifications, new products or services, sourcing, manufacturing, software development, technology procurement, trade secrets, bundling, and so forth. Your lean plan contains the decisions you make on these items as bullet points. You probably already know your tactics by heart, so all you have to do is list them briefly in your lean business plan.

Other Tactics. Tactics often include financial tactics, team building, hiring, recruitment tactics, or logistic tactics related to, say, taking on a new office or manufacturing space. Tactics are easier to recognize than define. Focus on content, and what’s supposed to happen. Think of tactics as absorbing the traditional marketing plan, product plan, and financing plan. Your next step will be to set these tactics into a plan with concrete milestones, performance metrics, lists of assumptions, and so on.

3. The Concrete Specifics.

Once you have the strategy and tactics clear, it’s the specifics you need to track progress, identify problems, and make changes. These include milestones, measurements, assumptions, and a schedule for regular review and revisions.

Review schedule. The single most important component of any real business plan—lean, traditional, or any other kind—is a review schedule. This sets the plan into the context of management. It makes it clear to everybody involved (even if that’s just you) that the plan is going to be reviewed and revised regularly. All the people charged with executing a business plan have to know when the plan will be reviewed, and by whom. This helps to make it clear that the plan will be a live management tool, not something to be put away on a shelf and forgotten.

Identify and List Assumptions. Identifying assumptions is extremely important for getting real business benefits from your business planning. Planning is about managing change, and in today’s world, change happens very fast. Assumptions solve the dilemma about managing consistency over time, without banging your head against a brick wall.

Assumptions might be different for each company. There is no set list. What’s best is to think about those assumptions as you build your twin action plans.

If you can, highlight product-related and marketing-related assumptions. Keep them in separate groups or separate lists. The key here is to be able to identify and distinguish later (during your regular reviews and revisions) between changed assumptions, and the difference between planned and actual performance. You don’t truly build accountability into a planning process until you have a good list of assumptions that might change.

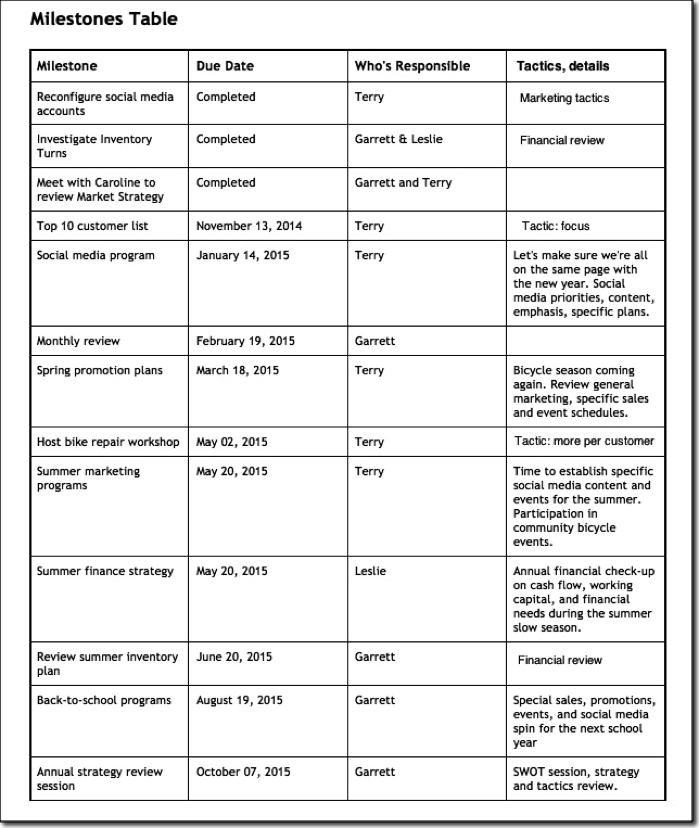

Milestones. There’s no real plan without milestones. Milestones are what you use to manage responsibilities, track results, and review and revise. And without tracking and review, there is no management and no accountability.

Just as you need tactics to execute strategy, so too do you need milestones to execute tactics. Normally you’ll look for a close match between tactics and milestones.

Take your milestones list and categorize what’s supposed to happen—and when—for ongoing tactics related to products, services, marketing, administration, and finance. These include launch dates, review dates, prototype availabilities, advertising, social media, website development, programs to generate leads, and traffic. These milestones set the plan tactics into practical, concrete terms, with real budgets, deadlines, and management responsibilities. They are the building blocks of strategy and tactics. And they are essential to your ongoing plan (vs. actual management and analysis), which is what turns your planning into management.

Give each milestone at least the following:

– Name

– Date

– Budget

– Person responsible

– Expected performance metric

– Relationship with specific tactics and strategy points

Figure 2.2 – Lean Plan Milestones

Metrics. Developing performance metrics is a critical part of developing accountability as one of the principles of lean planning. Make them an explicit part of your lean plan. Show them to the management team as part of your planning, and then show the results again and again during your monthly review meeting. Management often boils down to setting clear expectations and then following up on results. Those expectations are the metrics.

The most obvious metrics are in the financial reports: sales, cost of sales, expenses, and so on. However, with good lean planning, you can look for metrics throughout the business, aside from what shows up in the financial reports. For example, marketing generates metrics on websites, social media, emails, conversions, visits, leads, seminars, advertisements, media placements, and so on. Sales should track calls, visits, presentations, proposals, store traffic, price promotions, and so on. Customer service has calls, problems resolved, and other measures. Finance and accounting have metrics that include collection days, payment days, and inventory turnover. Business is full of numbers to manage and track performance. When metrics are built into a plan and shared with the management team, they generate more accountability and more management.

A going business is always revising its plan. Change is constant. Follow your review schedule monthly. A real business plan is never done. If your plan is done, your business is done.

Experts know that planning is managing change, and is not voided by change. As your business evolves, so will your business plan. You’ll add pieces to fit your needs. You’ll need to add product and marketing information to coordinate development, deployment, messaging, and timing. You’ll have to add to your financials to account for loans and capital equipment, which become part of a balance sheet.

The normal lean planning process is what Tim Berry calls the PRRR cycle—“plan, run, review, and revise.” It is lean planning version of the traditional lean business technique, and is one of the most critical tools in managing your high-growth startup.

The workable lean business plan is the first step in a planning process that will help you steer your business and optimize your management to be sure your business does what you want. Follow up with the review schedule: review plan vs actual results every month, and keep your plan alive and growing. Keep it lean, and keep it live.

This post is part of the “Prepare” series of the Gust Founder Curriculum. Gust’s Founder Curriculum is a roadmap for founders navigating every stage of the founder journey. Check out our event series and follow along with expanded resources here.

Get the guidance you need when setting up your company for investment.

This article is intended for informational purposes only, and doesn't constitute tax, accounting, or legal advice. Everyone's situation is different! For advice in light of your unique circumstances, consult a tax advisor, accountant, or lawyer.