Don’t Misunderstand Sweat Equity

Don’t misunderstand sweat equity. It’s a bucket term that means different things in different contexts. Fundamental sweat equity is beautiful, blisteringly clear, and real. Most other sweat equity is full of potential problems, misunderstandings, and disappointments.

In decades with startups — as a founder who raised angel investment and later as angel investor — I’ve seen a lot of different spins on so-called sweat equity. So I want to sort this out.

Real sweat equity

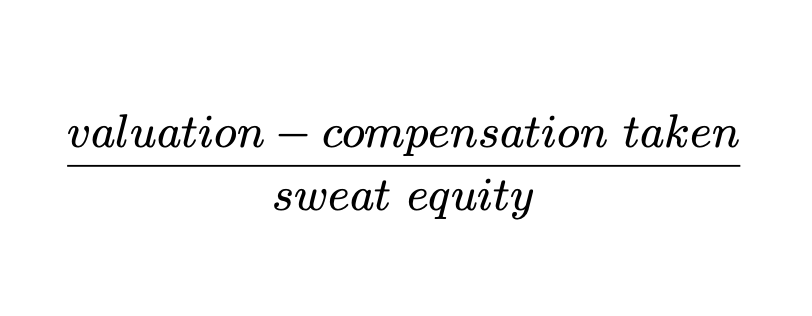

Real sweat equity is solid. You start your company, create something from nothing, grow it, and the sweat equity value is simple and obvious. For every company owned by its founder(s), sweat equity is a simple formula:

This is the way of the startup world, for the most part. Real life. Be careful, though, as you develop the business, not to underestimate real expenses and overstate profits by ignoring the fair value of the founder’s work. That messes up the analysis.

When I read business plans as a potential investor, I expect the founders to include the value of their work in the valuation. I don’t like it when they promise to work for less than fair value in the future because that puts pressure on the system. Sometimes those sacrifices blow up on the company at bad moments. I like a business that can afford to pay everybody working there, including founders. And if the numbers work, the future prospects are good, then that can be part of what investment funds are used for.

And I hate seeing liabilities on the balance sheet (see point 3, below) that track back to unpaid compensation for founders. Your valuation is your compensation.

Gust Launch can set your startup right so its investment ready.

The bad examples of sweat equity

However, a lot of so-called sweat equity isn’t solid; it’s like folded paper, easy to rip or crush, not reliable. Some examples:

1. Peanuts-and-promises sweat equity: Ralph hires Mary for a lot less than she’d be worth on the market, and a lot less than what it would cost him to get a market-value employee to do what Mary does. Time passes. Mary works. She thinks she owns 50% of the business. But nothing is written. The business takes off. Mary wants her share but now she’s asking, as a supplicant. Her share is whatever Ralph decides is fair. Ugly, but it happens a lot.

2. Salary-plus-shares sweat equity: This is way better than the peanuts and promises. There’s a formula and some specific numbers to it. Both sides negotiate the mix of money and shares. However, shares are just one number in a calculation that depends on two numbers; percent ownership is another simple formula:

Way too often people dangle shares as reward, without specifying total shares outstanding. It becomes another misunderstanding and disappointment waiting to happen.

3. Temporary-and-will-be-capitalized sweat equity: Founders work for less than fair value and record the difference between actual pay and fair value as owed to founders, a liability on the balance sheet. This has the advantage of recording real expenses into the financials, so I like it. But founders asking for outside investment should expect to capitalize that and swallow the liability. You can’t use founders’ labor to justify the valuation ask, and then turn around and get it paid too. You know: cakes and eating?

4. Plain exploitative BS sweat equity: It happens all the time. Whenever startup founders just get together and start working, without really agreeing on who owns how much, and who does what for how much, there’s a 90% or more chance somebody is going to end up shafted, feeling they’ve contributed more than their share and got less than their share back. I hate hearing about this. “You’re an owner” and “we’re partners” and “sure, I’ll take care of you” are incredibly powerful lures used way too often to get more work for less ownership and less money.

If you and your team are serious about your venture, check out Gust’s Co-founder Equity Split tool to better estimate a fair split of founder equity.

About

Tim Berry is the founder of Palo Alto Software, a co-founder of Borland International, and a recognized expert in business planning. Tim is the originator of Lean Business Planning. He has an MBA from Stanford and degrees with honors from the University of Oregon and the University of Notre Dame. Today, Tim dedicates most of his time to blogging, teaching and evangelizing for business planning. His full biography is available on his blog.

Gust Launch can set your startup right so its investment ready.

This article is intended for informational purposes only, and doesn't constitute tax, accounting, or legal advice. Everyone's situation is different! For advice in light of your unique circumstances, consult a tax advisor, accountant, or lawyer.