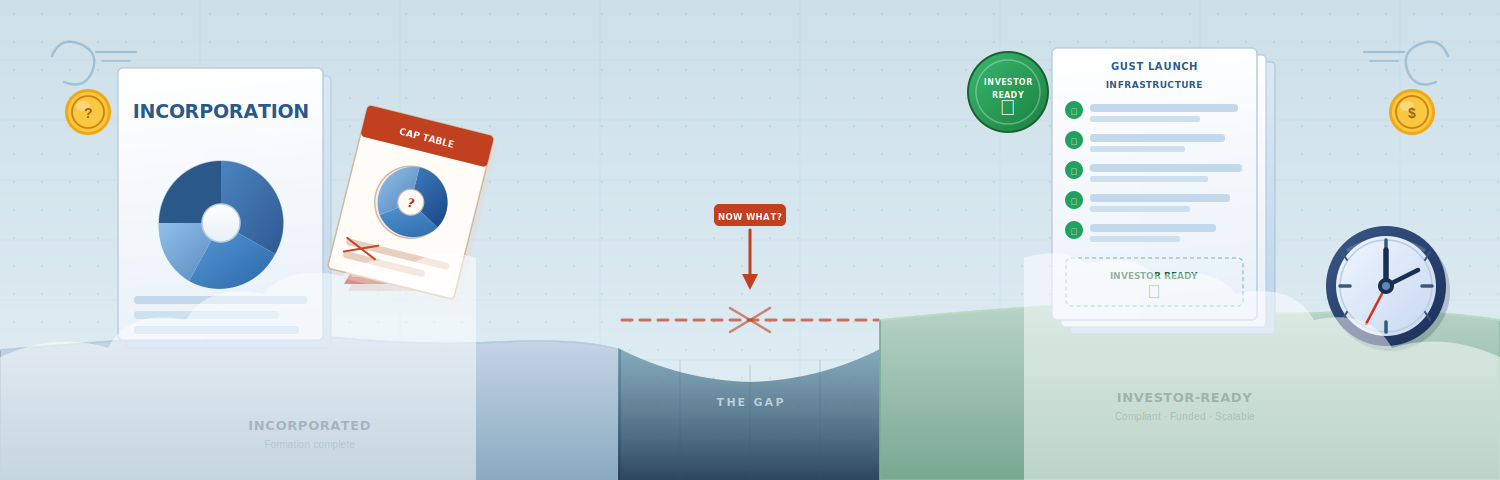

The Gap Between Incorporated and Investor-Ready

Getting incorporated as a Delaware C-corp is the right call if your goal is to grow fast, one day be acquired, or even go public. It’s the structure investors expect, the entity type that scales, and the foundation for equity, fundraising, and growth. If you’re already there, you made a smart decision. But here’s what most founders discover too late: incorporation is the starting line, not a finish line. The C-corp structure gives you the legal container but it doesn’t build what goes inside.

Robert Lee

, Operations

, Gust Inc

8 May 2026